| Taxwiz Accounting and Consulting Inc. | ||||||||

|

||||||||

|

|

| ||||||||||||||||||||

Tax Facts

The federal Minister of Finance revises premium rates of employment insurance and Canada Pension Plan, the federal base amount (i.e. the maximum amount of tax free income one could earn in a year), automobile deduction limits and reasonable expense rates of passenger vehicles for tax purposes every year. This web page summarizes vital tax related information in business decision making.

|

History of Canadian Income Tax |

|

Employment Insurance (EI)

|

Canada Pension Plan (CPP)

|

||||||||

| Year | EI rate |

Max. Wage Insurable |

Max. Employee Premium |

E/E ratio | CPP rate | Max. Wage Pensionable |

exemption |

Max. Employee

CPP Contribution |

E/E ratio |

| 1997 | 2.90% | $39,000 | $1,131 | 1.4 | 2.925% | $35,800 | $3,500 | $944.78 | 1.0 |

| 1998 | 2.70% | $39,000 | $1,053 | 1.4 | 3.2% | $36,900 | $3,500 | $1,068.80 | 1.0 |

| 1999 | 2.55% | $39,000 | $994.50 | 1.4 | 3.5% | $37,400 | $3,500 | $1,186.50 | 1.0 |

| 2000 | 2.40% | $39,000 | $994.50 | 1.4 | 3.9% | $37,400 | $3,500 | $1,329.90 | 1.0 |

| 2001 | 2.25% | $39,000 | $877.50 | 1.4 | 4.3% | $38,300 | $3,500 | $1,496.40 | 1.0 |

| 2002 | 2.20% | $39,000 | $858 | 1.4 | 4.7% | $39,100 | $3,500 | $1,673.20 | 1.0 |

| 2003 | 2.10% | $39,000 | $819 | 1.4 | 4.95% | $39,900 | $3,500 | $1,801.80 | 1.0 |

| 2004 | 1.98% | $39,000 | $772.20 | 1.4 | 4.95% | $40,500 | $3,500 | $1,831.50 | 1.0 |

| 2005 | 1.95% | $39,000 | $760.50 | 1.4 | 4.95% | $41,100 | $3,500 | $1,861.20 | 1.0 |

| 2006 | 1.87% | $39,000 | $729.30 | 1.4 | 4.95% | $42,100 | $3,500 | $1,910.70 | 1.0 |

| 2007 | 1.80% | $40,000 | $720 | 1.4 | 4.95% | $43,700 | $3,500 | $1,989.90 | 1.0 |

| 2008 | 1.73% | $41,100 | $711.03 | 1.4 | 4.95% | $44,900 | $3,500 | $2,049.30 | 1.0 |

| 2009 | 1.73% | $42,300 | $731.79 | 1.4 | 4.95% | $46,300 | $3,500 | $2,118.60 | 1.0 |

| 2010 | 1.73% | $43,200 | $747.36 | 1.4 | 4.95% | $47,200 | $3,500 | $2,163.15 | 1.0 |

| 2011 | 1.78% | $44,200 | $786.76 | 1.4 | 4.95% | $48,300 | $3,500 | $2,217.60 | 1.0 |

| 2012 | 1.83% | $45,900 | $839.97 | 1.4 | 4.95% | $50,100 | $3,500 | $2,306.70 | 1.0 |

| 2013 | 1.88% | $47,400 | $891.12 | 1.4 | 4.95% | $51,100 | $3,500 | $2,356.20 | 1.0 |

| 2014 | 1.88% | $48,600 | $913.68 | 1.4 | 4.95% | $52,500 | $3,500 | $2,425.50 | 1.0 |

| 2015 | 1.88% | $49,500 | $930.60 | 1.4 | 4.95% | $53,600 | $3,500 | $2,479.95 | 1.0 |

| 2016 | 1.88% | $50,800 | $955.04 | 1.4 | 4.95% | $54,900 | $3,500 | $2,544.30 | 1.0 |

| 2017 | 1.63% | $51,300 | $836.19 | 1.4 | 4.95% | $55,300 | $3,500 | $2,564.10 | 1.0 |

| 2018 | 1.66% | $51,700 | $858.22 | 1.4 | 4.95% | $55,900 | $3,500 | $2,593.80 | 1.0 |

| 2019 | 1.62% | $53,100 | $860.22 | 1.4 | 5.1% | $57,400 | $3,500 | $2,748.90 | 1.0 |

| 2020 | 1.58% | $54,200 | $856.36 | 1.4 | 5.25% | $58,700 | $3,500 | $2,898.00 | 1.0 |

| 2021 | 1.58% | $56,300 | $889.54 | 1.4 | 5.45% | $61,600 | $3,500 | $3,166.45 | 1.0 |

| 2022 | 1.58% | $60,300 | $952.74 | 1.4 | 5.70% | $64,900 | $3,500 | $3,499.80 | 1.0 |

| 2023 | 1.63% | $61,500 | $1,002.45 | 1.4 | 5.95% | $66,600 | $3,500 | $3,754.45 | 1.0 |

| 2024 | 1.66% | $63,200 | $1049.12 | 1.4 | 5.95% CPP2 rate 4% |

$68,500 CPP2 max $73,200 |

$3,500 | $3,867.50 CPP2 max $188 |

1.0 |

| 2025 | 1.64% | $65,700 | $1,077.48 | 1.4 | 5.95% CPP2 rate 4% |

$71,300 CPP2 max $81,200 |

$3,500 | $4,034.10 CPP2 max $396 |

1.0 |

| 2026 | 1.63% | $68,900 | $1,123.07 | 1.4 | 5.95%

CPP2 rate % |

$74,600 CPP2 max $ |

$3,500 | $4,230.45 CPP2 max $ |

1.0 |

| 2027 | % | $ | $ | 1.4 | %

CPP2 rate % |

$ CPP2 max $ |

$3,500 | $ CPP2 max $ |

1.0 |

Beginning 1 January 2024, employers must deduct the second additional CPP contributions (CPP2) on earnings above the annual maximum pensionable earnings using the following rates and maximums indicated above.

For more information, please read Changes in Canada Pension Plan (CPP).| Cost per $100 wage (EI & CPP)

subject to the max. EI & CPP contribution above |

Cost per $100 wage (CPP only)

subject to the max. CPP contribution above |

Cost per $100 wage (EI only)

subject to the max. EI contribution above |

Max WCB

insurable income/head |

||||

| Year | Employer | Employee | Employer | Employee | Employer | Employee | |

| 1997 | $6.99 | $5.83 | $2.93 | $2.93 | $4.06 | $2.90 | |

| 1998 | $6.98 | $5.90 | $3.20 | $3.20 | $3.78 | $2.70 | |

| 1999 | $7.07 | $6.05 | $3.50 | $3.50 | $3.57 | $2.55 | |

| 2000 | $7.26 | $6.30 | $3.90 | $3.90 | $3.36 | $2.40 | |

| 2001 | $7.45 | $6.55 | $4.30 | $4.30 | $3.15 | $2.25 | |

| 2002 | $7.78 | $6.90 | $4.70 | $4.70 | $3.08 | $2.20 | |

| 2003 | $7.89 | $7.05 | $4.95 | $4.95 | $2.94 | $2.10 | $60,100 |

| 2004 | $7.72 | $6.93 | $4.95 | $4.95 | $2.77 | $1.98 | $60,700 |

| 2005 | $7.68 | $6.90 | $4.95 | $4.95 | $2.73 | $1.95 | $61,300 |

| 2006 | $7.57 | $6.82 | $4.95 | $4.95 | $2.62 | $1.87 | $61,984 |

| 2007 | $7.47 | $6.75 | $4.95 | $4.95 | $2.52 | $1.80 | $64,400 |

| 2008 | $7.37 | $6.68 | $4.95 | $4.95 | $2.42 | $1.73 | $66,500 |

| 2009 | $7.37 | $6.68 | $4.95 | $4.95 | $2.42 | $1.73 | $68,500 |

| 2010 | $7.37 | $6.68 | $4.95 | $4.95 | $2.42 | $1.73 | $71,200 |

| 2011 | $7.44 | $6.73 | $4.95 | $4.95 | $2.49 | $1.78 | $71,700 |

| 2012 | $7.51 | $6.78 | $4.95 | $4.95 | $2.56 | $1.83 | $73,700 |

| 2013 | $7.58 | $6.83 | $4.95 | $4.95 | $2.63 | $1.88 | $75,700 |

| 2014 | $7.58 | $6.83 | $4.95 | $4.95 | $2.63 | $1.88 | $77,900 |

| 2015 | $7.58 | $6.83 | $4.95 | $4.95 | $2.63 | $1.88 | $78,600 |

| 2016 | $7.58 | $6.83 | $4.95 | $4.95 | $2.63 | $1.88 | $80,600 |

| 2017 | $7.23 | $6.58 | $4.95 | $4.95 | $2.28 | $1.63 | $81,900 |

| 2018 | $7.27 | $6.61 | $4.95 | $4.95 | $2.32 | $1.66 | $82,700 |

| 2019 | $7.37 | $6.72 | $5.10 | $5.10 | $2.27 | $1.62 | $84,800 |

| 2020 | $7.46 | $6.83 | $5.25 | $5.25 | $2.21 | $1.58 | $87,100 |

| 2021 | $7.66 | $7.03 | $5.45 | $5.45 | $2.21 | $1.58 | $100,000 |

| 2022 | $7.91 | $7.28 | $5.70 | $5.70 | $2.21 | $1.58 | $108,400 |

| 2023 | $8.23 | $7.58 | $5.95 | $5.95 | $2.28 | $1.63 | $112,800 |

| 2024 | $8.27 | $7.61 | $5.95 | $5.95 | $2.32 | $1.66 | $116,700 |

| 2025 | $8.25 | $7.59 | $5.95 | $5.95 | $2.30 | $1.64 | $121,500 |

| 2026 | $8.23 | $7.58 | $5.95 | $5.95 | $2.28 | $1.63 | $127,500 |

| 2027 | $ | $ | $ | $ | $ | $ | $ |

Many taxable allowances and benefits are subject to CPP and EI deductions. Furthermore, GST/HST has to be included in the value of the taxable benefit for income tax purposes.

Generally, payroll remittance due on or before the 15th of the following month after wages are paid except the following two accelerated payroll remitters:

Employers, including those with associated companies and multiple payroll accounts, who had a total average monthly withholding amount of $15,000 to $49,999.99 two calendar years ago must remit payroll remittance by the following dates:

Employers, including those with associated companies and multiple payroll accounts, who had a total average monthly withholding amount of $50,000 over more two calendar years ago must remit payroll remittance to a Canadian financial institution no later than the 3rd working day (excluding Saturdays, Sundays and public holidays) after the end of the following periods:

| Year | Base Amount (Fed) | Base Amount (BC) | Spouse/Dependent Amount (Fed) |

Spouse/Dependent Amount (BC) |

Max RRSP

Contribution Limit |

| 1997 | $6,456 | $13,500 | |||

| 1998 | $6,456 | $13,500 | |||

| 1999 | $6,794 | $13,500 | |||

| 2000 | $7,231 | $13,500 | |||

| 2001 | $7,412 | $6,293 | $13,500 | ||

| 2002 | $7,634 | $8,168 | $6,482 | $6,994 | $13,500 |

| 2003 | $7,756 | $8,307 | $6,586 | $14,500 | |

| 2004 | $8,012 | $8,523 | $6,803 | $7,298 | $15,500 |

| 2005 | $8,148 | $8,676 | $6,919 | $7,429 | $16,500 |

| 2006 | $9,039 | $8,858 | $7,675 | $7,585 | $18,000 |

| 2007 | $8,929 | $9,027 | $8,340 | $7,729 | $19,000 |

| 2008 | $9,600 | $9,189 | $9,600 | $7,868 | $20,000 |

| 2009 | $10,375 | $9,373 | $10,375 | $8,026 | $21,000 |

| 2010 | $10,382 | $11,000 | $10,382 | $9,653 | $22,000 |

| 2011 | $10,527 | $11,088 | $10,527 | $9,730 | $22,450 |

| 2012 | $10,822 | $11,354 | $10,822

($12,822 if infirmed) |

$9,964 | $22,970 |

| 2013 | $11,038 | $10,276 | $11,038

($13,078 if infirmed) |

$8,860 | $23,820 |

| 2014 | $11,138 | $9,869 | $11,138

($13,196 if infirmed) |

$8,450 | $24,270 |

| 2015 | $11,327 | $9,938 | $11,327

($13,420 if infirmed) |

$8,509 | $24,930 |

| 2016 | $11,474 | $10,027 | $11,474

($13,595 if infirmed) |

$8,586 | $25,370 |

| 2017 | $11,635 | $10,208 |

$11,635

($13,785 if infirmed) |

$8,740 | $26,010 |

| 2018 | $11,809 | $10,412 | $11,809

($ if infirmed) |

$8,915 | $26,230 |

| 2019 | $12,069 | $10,682 | $12,069

($14,299 if infirmed) |

$9,147 | $26,500 |

| 2020 | $12,298 | $10,949 |

$12,298

($14,571 if infirmed) |

$9,376 | $27,230 |

| 2021 | $13,808 | $11,070 | $13,808 ($16,103 if infirmed) |

$9,479 | $27,830 |

| 2022 | $14,398 | $11,302 | $14,398 ($16,748. if infirmed) |

$9,678 | $29,210 |

| 2023 | $15,000 | $11,981 | $15,000 ($17,499 if infirmed) |

$10,259 | $30,780 |

| 2024 | $15,705 | $12,580 | $15,705 ($18,321 if infirmed) |

$10,772 | $31,560 |

| 2025 | $16,129 | $12,932 | $16,129 ($18,816 if infirmed) |

$11,073 | $32,490 |

| 2026 | $16,452 | $13,216 | $16,452 ($19,192 if infirmed) |

$11,317 | $33,810 |

| 2027 | $ | $ | $ ($ if infirmed) |

$ | $35,390 |

The threshold column above contains a lower limit and a upper limit (separated by a slash "/"). Within the range defined by these limits, the amount of spouse amount will be reduced by the amount of income the spouse or the dependent earned. Under the lower limit, there is no reduction of spouse amount, whereas the spouse amount ceases to exist once the upper limit is exceeded.

The maximum RRSP contribution limit is created by 18% of the earned income. At the point of writing, there is no limit restricting the deduction of accrued unused RRSP limit from taxable income in a year.

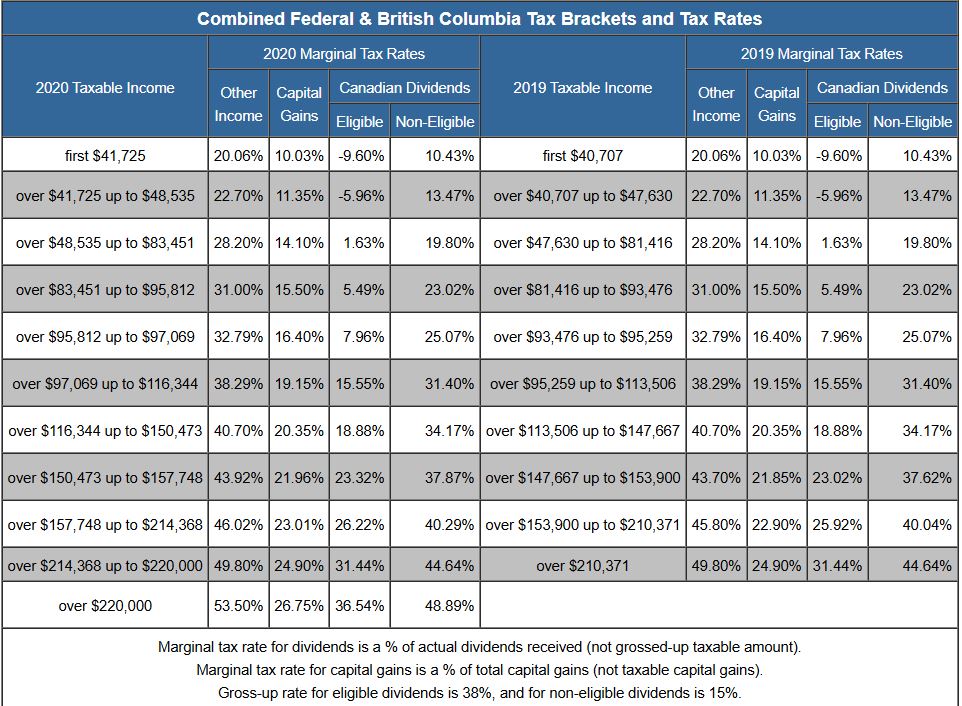

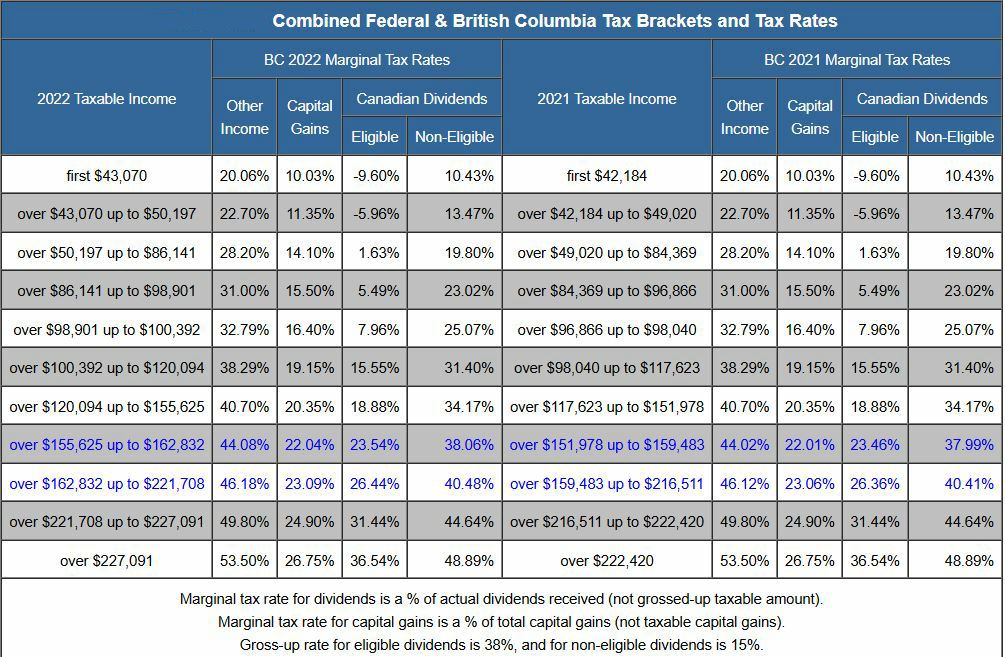

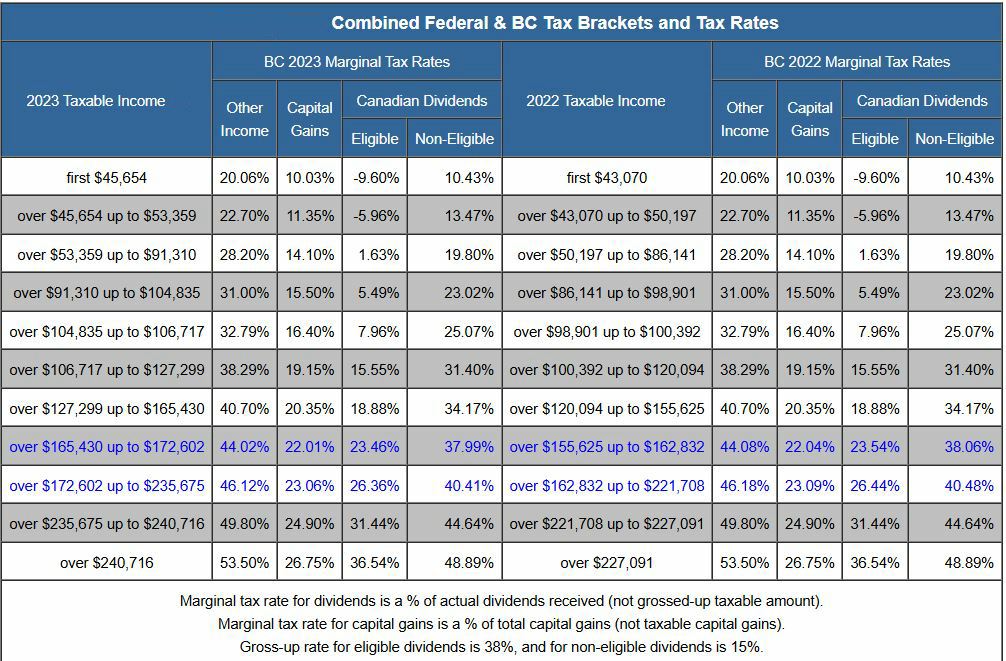

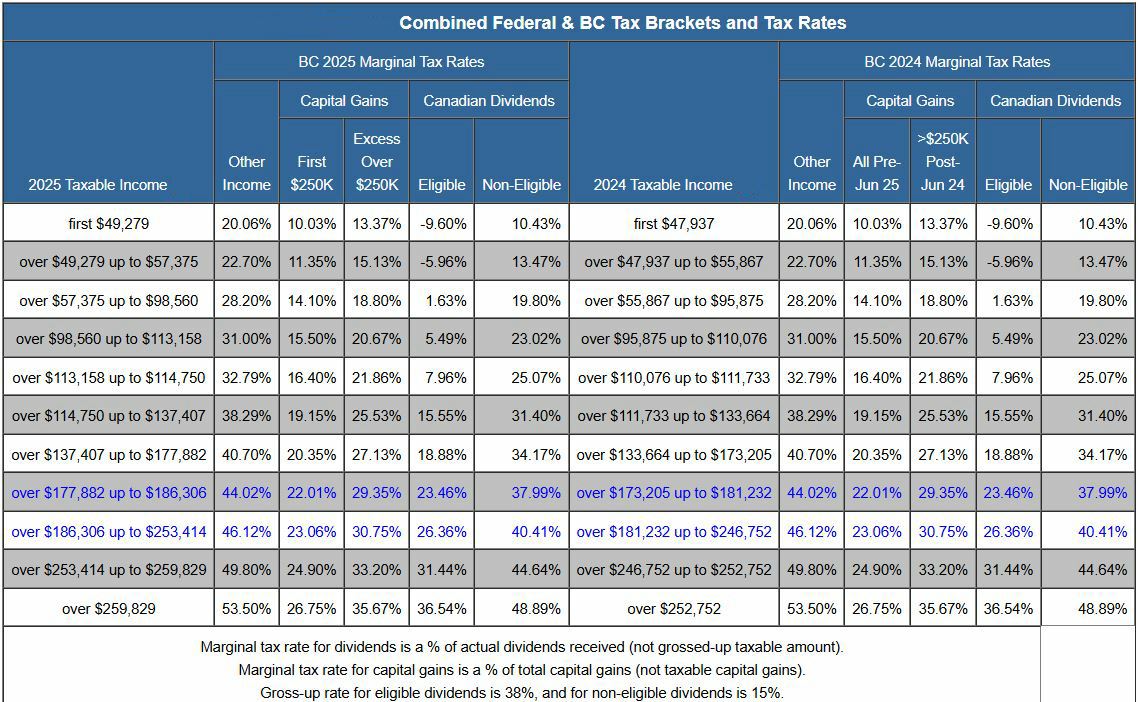

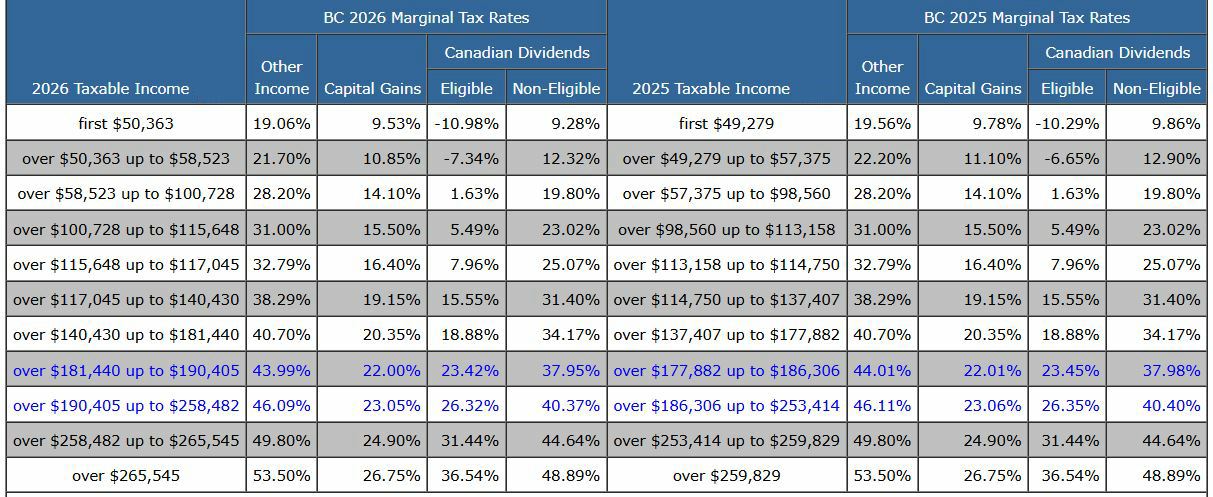

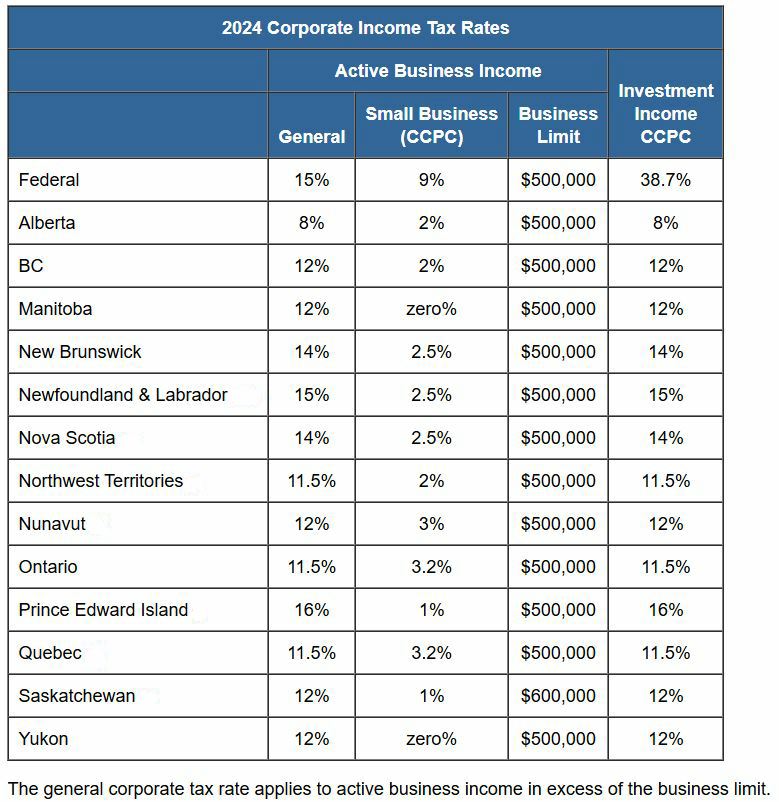

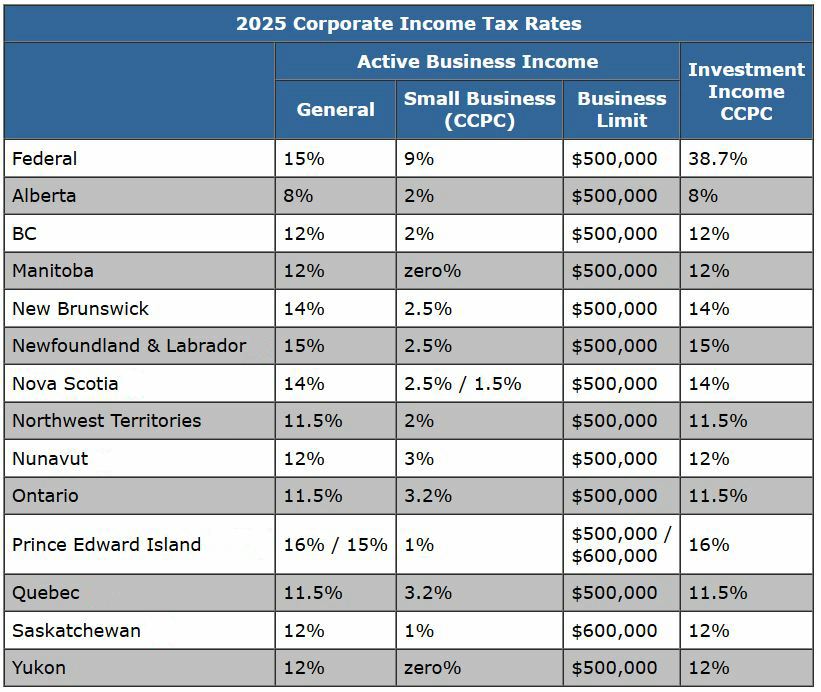

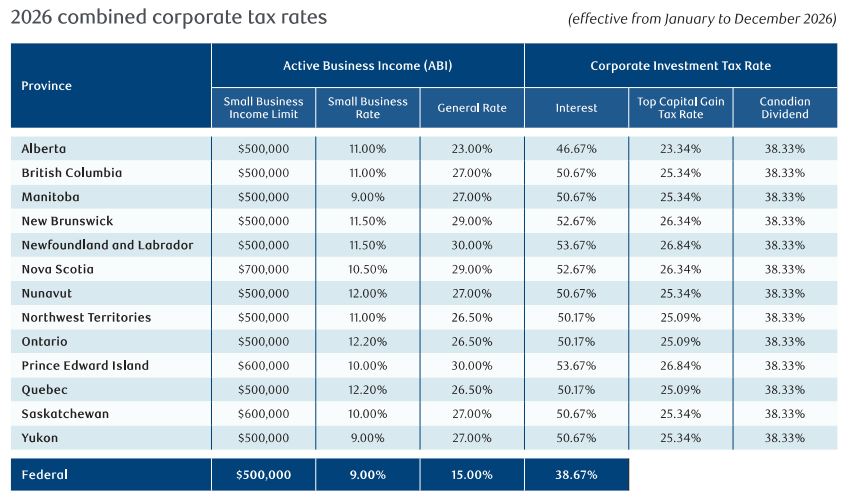

Both federal and provincial/territorial governments levy tax on worldwide income earned by individuals and corporations at different marginal tax rates for various taxable income level. In this progressive tax regime, marginal income tax rates and taxable income brackets could change each year after the budgets are announced. Starting from 2009, these rates (British Columbia's only) are summarized in the following table.

Personal Income Tax Rates |

Corporate Income Tax Rates |

||||||||||||

|

Federal and provincial income taxes are subject to exemption of the base amounts indicated in the table under the heading "Federal/British Columbia Base Amount and Maximum RRSP Contribution Limit".

Please click the year below to view rates in that year.

20092010201120122013201420152017201920202021-222023202420252026 |

|||||||||||||

Income Tax Return Filing Due Date[Note that Income Tax Return Filing Due Date and Tax Balance Due Date are different.] |

|||||||||||||

|

Personal income tax returns are generally due on the 30th of April each year. For self-employed persons, if the taxpayer or his/her spouse or common-law partner carried on a business in the following year (other than a business whose expenditures are primarily in connection with a tax shelter), personal tax return has to be filed on or before 15 June the following year. However, if you have a balance owing, you still have to pay it on or before 30 April the following year. Final Return for Deceased Persons Generally, the final return is due on or before the following dates:

Note The due date for filing the T1 return of a surviving spouse or common law partner who was living with the deceased is the same as the due date for the deceased's final return indicated in the chart above. However, any balance owing on the surviving spouse's or common law partner's return still has to be paid on or before April 30 of the next year to avoid interest charges. If the deceased or the deceased's spouse or common-law partner was carrying on a business in 2012 (unless the expenditures made in the course of carrying on the business were mainly the cost or capital cost of tax shelter investments), the following due dates apply:

|

Corporate tax return due for filing 6 months after the fiscal year end each fiscal period. When the corporation's tax year ends on the last day of a month, file the return by the last day of the sixth month after the end of the tax year. When the last day of the tax year is not the last day of a month, file the return by the same day of the sixth month after the end of the tax year. When the T2 filing deadline falls on a Saturday, Sunday, or statutory holiday, CRA will consider the return filed on time if it is sent on the first business day after the filing deadline. Note Corporations with no business activities, including newly incorporated companies which never operate, are required to file a corporate income tax return each year. |

||||||||||||

Income Tax Balance Due Date |

|||||||||||||

|

Personal income tax balance due are due on the 30th of April each year. The due date for a balance owing on a final return depends on the date of death.

In some cases, the legal representative of the deceased taxpayer may make an election to delay paying part of the amount due. For instance, paying part of the amount owing from rights or things and the deemed disposition of capital property may be delayed. |

Generally, all corporation taxes (with the exception of Part III and Part XII.6) are due two months after the end of the tax year. However, the tax is due three months after the end of the tax year if the following conditions apply:

Sections 125 and 157 of the Income Tax Act |

||||||||||||

Taxpayers, corporate and individual alike, are not required to pay instalment tax on the following taxes if their tax payable is below the following thresholds:

Corporations with tax payable exceeding this threshold must pay corporate income tax instalments according to the following:

using one of the options below:

New Corporations

Except for Part XII.I tax, you do not have to make instalment payments for a new corporation until you have started your second year of operation. However, for your first year of operation, you have to pay any tax you owe on or before your balance due date for that tax year.

If your business is located in either Ontario or British Columbia and you have an annual reporting period that begins in 2010 with an HST payable exceeding the threshold, there are proposed changes for calculating the amount of your HST instalment payments for that reporting period. Your instalment payments that become payable after the first fiscal quarter beginning on or after July 1, 2010, will be equal to the lesser of ?of the amount of net tax for the current year and ?of 240% of the amount of the net tax for the previous year.

Quarterly HST/GST installment payments are due one month after the end of each of your fiscal quarters and are usually equal to a quarter (? of your net tax from the previous year. You may also choose to base your quarterly installment payments on an estimate of your net tax for the current year if you expect that it will be less than it was for the previous year.

If your GST/HST payment is $50,000 or more, you must pay it electronically or at your financial institution, not by mail or in person to CRA, on or before the due date.

GST/HST Filing Frequency

GST/HST filing frequency is determined by the amount of annual gross income of a taxpayer:

Automobile Allowance Rates and Passenger Vehicle Tax Related Limits

| Automobile Allowance Rates in Most of Canada | general prescribed rate for taxable car benefit |

CCA ceiling

for Class 10.1 passenger vehicles (before sales taxes) |

monthly limit

on deductible leasing costs (before sales taxes) |

max monthly

deductible car loan interest |

||

| first 5,000 km |

each additional

km thereafter |

|||||

| Year | ||||||

| 1998 | $25,000 | $550 | ||||

| 1999 | $0.35 | $0.29 | $26,000 | $650 | $250 | |

| 2000 | $0.37 | $0.31 | $27,000 | $700 | $250 | |

| 2001 | $0.41 | $0.35 | $30,000 | $800 | $300 | |

| 2002 | $0.41 | $0.35 | $0.16 | $30,000 | $800 | $300 |

| 2003 | $0.42 | $0.36 | $0.17 | $30,000 | $800 | $300 |

| 2004 | $0.42 | $0.36 | $0.17 | $30,000 | $800 | $300 |

| 2005 | $0.45 | $0.39 | $0.20 | $30,000 | $800 | $300 |

| 2006 | $0.50 | $0.44 | $0.22 | $30,000 | $800 | $300 |

| 2007 | $0.50 | $0.44 | $0.22 | $30,000 | $800 | $300 |

| 2008 | $0.52 | $0.46 | $0.24 | $30,000 | $800 | $300 |

| 2009 | $0.52 | $0.46 | $0.24 | $30,000 | $800 | $300 |

| 2010 | $0.52 | $0.46 | $0.24 | $30,000 | $800 | $300 |

| 2011 | $0.52 | $0.46 | $0.24 | $30,000 | $800 | $300 |

| 2012 | $0.53 | $0.47 | $0.26 | $30,000 | $800 | $300 |

| 2013 | $0.54 | $0.48 | $0.27 | $30,000 | $800 | $300 |

| 2014 | $0.54 | $0.48 | $0.27 | $30,000 | $800 | $300 |

| 2015 | $0.55 | $0.49 | $0.27 | $30,000 | $800 | $300 |

| 2016 | $0.54 | $0.48 | $0.26 | $30,000 | $800 | $300 |

| 2017 | $0.54 | $0.48 | $0.25 | $30,000 | $800 | $300 |

| 2018 | $0.55 | $0.49 | $0.26 | $30,000 | $800 | $300 |

| 2019 | $0.58 | $0.52 | $0.28 | $30,000 | $800 | $300 |

| 2020 | $0.59 | $0.53 | $0.28 | $30,000 ($55,000 for eligible zero-emission passenger vehicles) | $800 (A separate restriction prorates deductible lease costs where the value of the vehicle exceeds the capital cost ceiling of $30,000.) | $300 |

| 2021 | $0.59 | $0.53 | $0.27 |

$30,000 ($55,000 for eligible zero-emission passenger vehicles) |

$800 | $300 |

| 2022 | $0.61 | $0.55 | $0.29 |

$34,000 ($59,000 for eligible zero-emission passenger vehicles) |

$900 | $300 |

| 2023 | $0.68 | $0.62 | $0.33 | $36,000

($61,000 for eligible zero-emission passenger vehicles) |

$950 | $300 |

| 2024 | $0.70 | $0.64 | $0.33 |

$37,000 ($61,000 for eligible zero-emission passenger vehicles) |

$1,050 | $350 |

| 2025 | $0.72 | $0.66 | $0.34 |

$38,000

($61,000 for eligible Class 54 zero-emission passenger vehicles) |

$1,100 | $350 |

| 2026 | $0.73 | $0.67 | $0.34 |

$39,000

($61,000 for eligible Class 54 zero-emission passenger vehicles) |

$1,100 | $350 |

| 2027 | $ | $ | $ |

$

($ for eligible Class 54 zero-emission passenger vehicles) |

$ | $ |

Yukon, Northwest Territories & Nunavut have a slightly higher automobile allowance rates than those for the rest of Canada. Please contact Taxwiz Accounting if you need these rates.

In addition to the operating cost portion calculated on a per kilometer basis, the taxable automobile benefits also include a standby charge. Automobile benefits are not insurable (hence no EI premium is required) but subject to CPP and income tax withheld.

Exchange Rates

For tax purposes, CRA accepts the average exchange rates published by the Bank of Canada in converting foreign currencies to Canadian dollar. The following table contains some major exchange rates (rounded to the 4th decimal) extracted from data published by the Bank of Canada since 1999.

CRA uses prescribed interest rates to compute interest charged on amounts owed and interest paid to taxpayers on amounts the CRA owes to individuals and corporations. These rates are revised every quarter and are linked herein.